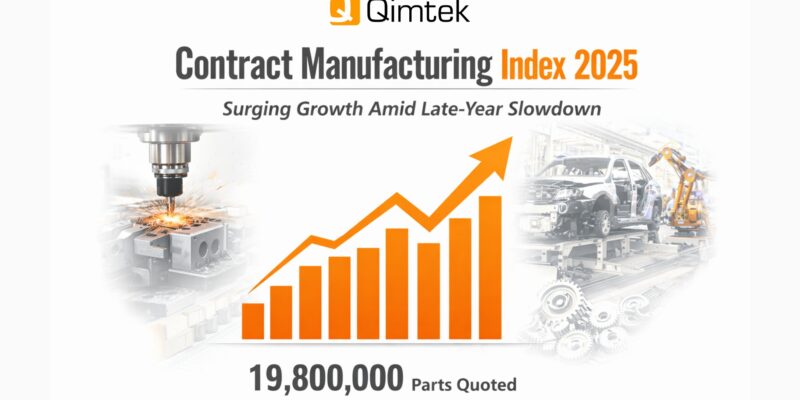

The Contract Manufacturing Index (CMI) recorded a strong rebound in 2025, with the annual index rising 47% above 2024 averages, signalling renewed momentum across the subcontract manufacturing market.

Based on data from 427 companies and 1,254 projects, the index shows that demand remained well ahead of last year, even as activity cooled in the final quarter. While the fourth quarter index fell 39% compared to Q3, it still stood an impressive 64% higher than the same period in 2024. The year also saw a sharp rise in quoting activity, with nearly 19.8 million parts processed on the platform.

Machining continued to dominate outsourcing demand, accounting for the majority of projects and delivering steady year-on-year growth, while fabrication and emerging “other” processes showed notable gains in value. Across the board, suppliers became more cautious toward the end of the year, with uncertainty around the delayed budget dampening late-quarter momentum.

Despite this, operational efficiency improved. Average supplier lead times fell to 19 days, down from 20 days in 2024, continuing a steady downward trend.

Industry performance shifted throughout the year, with Automotive leading overall activity, while Industrial Machinery reclaimed the top spot in the final quarter. These movements underline a market that is adapting quickly to disruption while maintaining strong underlying demand.

The full CMI report breaks down these trends in detail, offering deeper insight by process, industry, and quarter, and highlighting what they mean for buyers and suppliers heading into 2026.

https://www.qimtek.co.uk/blog/contract-manufacturing-index-2025