In an era of rising costs from labour shortages and supply chain challenges, timely access to data is essential. Static spreadsheets used for estimating and tracking costs need to be replaced by dynamic data management, such as enterprise resource planning systems that incorporate historical, tribal knowledge with the collection and analysis of current data. The goal is to generate consistent estimates and provide profitable, competitive pricing – MIE Solutions explains.

Estimating fundamentals matter, especially now. Numerous factors influence the cost to produce parts, and understanding the basics of shop rates and sell rates is critical to determine a sell price that is both competitive and profitable.

How to Calculate the Shop Rate

Shop rates are the costs incurred for the production of parts on an hourly basis. To determine shop rates, first identify your direct hourly labor rates, your fixed overhead costs, and your variable overhead costs.

Direct hourly labour rates are the easiest to establish. They’re simply based on the actual hourly wage paid to employees. To determine the direct hourly labour rate for each production department, add the hourly wage rate for each department employee and then divide that by the total number of employees. This gives you the average hourly rate.

Most companies will then round that up. If your average rate were £12.35 per hour, you might round that to £12.50 or £13.00. Be sure to calculate the direct hourly labour rate for each production department, each of which has varying degrees of expertise among trained employees.

You also might consider identifying a rate for setup. Some machines may require more experienced employees for setup, but once they produce the first article, a less experienced employee can run the parts.

You could even establish direct hourly labour rates based on job type, such as prototype versus production or standard run versus expedited. Typically, a more experienced employee will produce prototypes, and a shop will charge higher rates for expedited production.

Overhead rates are more difficult to establish. Some just establish a single overhead rate for the facility, while others develop rates for each production department. After all, the costs behind every process—cutting, bending, deburring, machining, welding, or other anything else—can vary. Some machines may be fully depreciated while other machines are brand new and are just starting to be depreciated or have a lease payment each month. Power consumption can vary as well, and some equipment may require more maintenance.

Developing overhead rates for each production department lets you see the true cost of running the operation and allows you to be more competitive in your pricing. To develop overhead rates by production department, you need to look at both fixed and variable overhead expenses.

Fixed overhead costs are incurred whether the facility is up and running or shut down. Examples would be rent, equipment leases, utilities, and depreciation. Calculating these for the entire facility is straightforward; determining fixed overhead costs for each production department is a little more complex.

Using the most recent 12 months of data, you may allocate costs to each production department based on square footage (rent, utilities) or equipment costs (equipment leases and/or depreciation). Once you have the total costs allocated to each production department, determine the hourly cost by dividing the total by the estimated productive hours for the next 12 months. This will give you the fixed overhead costs by hour for each production department.

Variable overhead costs are directly related to the production of revenue-generating parts. Examples would be consumables such as welding gases, welding wire or rod, safety equipment, and indirect labor. These expenses vary with increases or decreases in production.

Again, using data from the past 12 months, you can allocate costs to the corresponding production department. Because we’re in an inflationary period, you’ll want to increase these total costs based on expected increases over the next 12 months. You then divide a department’s total costs by the estimated productive hours for the next 12 months, giving you the variable overhead costs by hour for each production department.

Estimated productive hours is the time equipment is expected to produce revenue-generating parts. A one-shift operation, eight hours per day, five days per week, has 2,080 hours worked in a year. Of course, employees don’t work for 2,080 hours. They take breaks, as required by law, they go on vacation and sick leave, and they have company holidays. And sometimes an employee is out, leaving no one available to operate a machine. Additionally, some departments may not be fully utilized over the course of 12 months.

Once you determine the percentage of time a department will be productive, multiply that percentage by the 2,080 hours (or more, if you’re running multiple shifts) to determine the estimated productive hours for that department. So, a department that works 80% of the time would have 1,664 estimated productive hours a year (2,080 × 0.80).

For production departments with multiple machines, estimated productive hours would incorporate the sum of all of them. Say you have three lasers in your cutting department, and the estimated productive hours for each is 1,664. So, the total productive hours per year for the department would be 1,664 × 3, or 4,992 hours.

Now that you have determined your direct hourly labor rate, fixed overhead hourly costs, and variable overhead hourly costs, you can add those together to calculate your hourly shop rate for each production department.

Sell Rate and Sell Price

The sell rate for each production department helps determine the price for the production time of parts. In reality, the sell rate is a function of what the market will bear. Based on the market sell rate for each production department, you can determine the profit using the shop rates that you calculated previously.

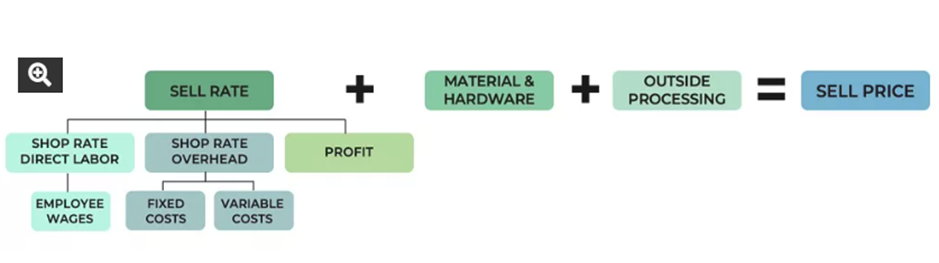

For each production area, the estimated profit would be the market sell rate less the shop rate. The sell price is the price at which the company is willing to produce and deliver parts. It includes the sell rate plus the cost of materials and outside processing (see Figure 1).

Some operations want all costs to be fully absorbed for estimating purposes. In these cases, they give estimates that incorporate operational overhead costs. These non-inventoriable costs include non-revenue-generating expenses likes sales, marketing, administration, and accounting.

To determine the hourly operational overhead cost, you again would utilize the most recent 12 months of cost data for these areas and divide the total by the total estimated productive hours for all production departments. Add the hourly operational overhead cost to the sell price and you get the fully burdened sell price.

Developing Estimated Times

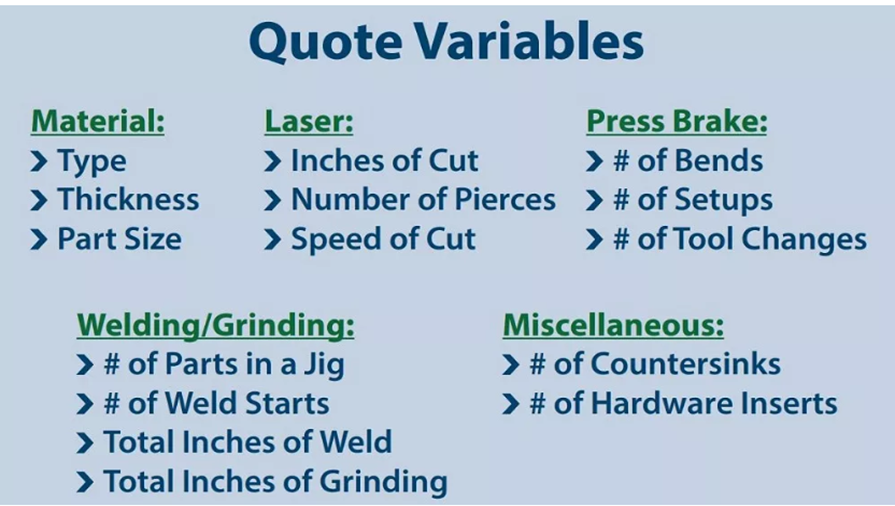

Identifying and calculating the sell rate for a production department is just one component of providing an estimate. A more critical piece is the estimated time it will take to actually produce the part. Variables include the type of material, material thickness, part size, internal geometry, hardware, number and type of bends, part finish, and any other processing variable that affects the time needed to complete a job. Just as you developed hourly rates for each production department, you can also develop standard formulas that incorporate these variables to estimate the time required. Using standard formulas in conjunction with your sell rate will produce consistent estimates regardless of the estimator. For example, a bending formula might incorporate not only the number of bends of a particular part, but also the number of part flips, factoring in part size and the need for helpers.

When using a standard formula for a laser, an estimator would only be required to enter material thickness, type of material, total inches of cut, and number of pierces. The formula will then provide the estimated run time.

Exact formulas can vary depending on the operation, and they can evolve over time. For instance, a formula for laser cutting might start with (Linear inches of cut/speed of cut in IPM) + (Number of pierces × Pierce time/60). Estimators would then multiply the result with the department’s hourly shop rates for direct labor and overhead. As quoting evolves, other variables might be added to the formula, such as part removal time, whether the operation is automated or involves a helper hammering a thick part out of a skeleton. A cut sheet on an offload table might not tie up machine resources, but there are still labor costs associated with removing and organizing those parts, and, depending on the operation, an estimator might want to account for them.

Setup times typically are standardized by production department, and most rely on default times unless there is an overly complex or simple part. Estimators usually divide setup time by quantity and multiply that by the department’s hourly rate (though the direct labor shop rate might be higher, depending on the setup personnel involved). The shorter the setup, the more competitive a shop can be on low-quantity runs.

The idea is to get the estimated time as close to the actual time as you possibly can—a feat that (as we’ll discuss soon) makes an entire operation more flexible and competitive (see Figure 2). And when you use an ERP system, instead of traditional spreadsheets, you can maintain all of the labor and overhead rates as well as the standard formulas in one place, facilitating easy updates and access by all estimators.

Actual Versus Estimated

Being able to compare the actual time and costs during production to the original estimate allows you to evaluate employee performance, the validity of standard formulas, material utilization, and overhead absorption. When you see a variance, you can adjust pricing as needed for future orders.

By tracking and comparing the actual versus estimated direct labor time for each operation, you evaluate estimating accuracy and employee efficiency. Longer-than-estimated labor time could indicate a problem, such as excessive scrap parts and rework. Work instructions might be vague, employees might need more training, or the estimate (including the standard formula it relies on) might simply be inaccurate. If employees performed efficiently and the operation went smoothly, you might need to reevaluate the standard formula and adjust it as needed.

Next comes material utilization. Was the actual yield greater or less than estimated? Evaluate the variance, determine the cause, and adjust as necessary for future quotes.

Actual versus estimated comparisons also affect overhead absorption. If a job takes less time than estimated, it absorbs less overhead and realizes greater profit. Conversely, if it took more time than expected, it absorbs more overhead and puts profit at risk.

Evaluate overhead rates quarterly, and make sure they incorporate changes in equipment utilization, actual hours utilized, and actual expenses incurred. By continually monitoring and adjusting overhead rates, you help make sure you don’t under- or over-absorb these costs.

The actual-versus-estimated comparison allows you to continuously refine the rates, times, and formulas estimators use. Put simply, accurate quoting helps you maintain consistent profits.

In highly competitive environments or during times of economic downturn, knowing precise costs allows you to understand how far you can reduce pricing to keep the lights on without losing money. This can mean the difference between keeping trained employees or being faced with difficult workforce reductions.

Say your company has reached its productive capacity. If you know the precise costs and the profits produced by a job, you can reevaluate pricing on lower-margin items and increase sell prices accordingly.

The ability to estimate the cost of production accurately may make the difference between success and failure in today’s competitive manufacturing landscape. Estimating the cost of a job or service requires a firm understanding of the part, its production history, the time required to produce it, and the associated costs of labor and materials.

Accurately identifying the associated costs ensures that each production order adheres to the company’s business model and desired margin. For decades, manufacturing has survived using tribal knowledge, pen and paper, spreadsheets, and printed documents to quote business. These slow, archaic methods may have worked in the past, but they won’t in the future. Here, modern software platforms are playing an increasingly critical role, helping shops streamline the calculation of job costing and estimating. This helps keep profits consistent and, ultimately, makes a fabricator more competitive as it navigates the ever-changing economic landscape.