Subcontract market up 4.5% on previous quarter

Order pipeline unblocked as new projects come onstream

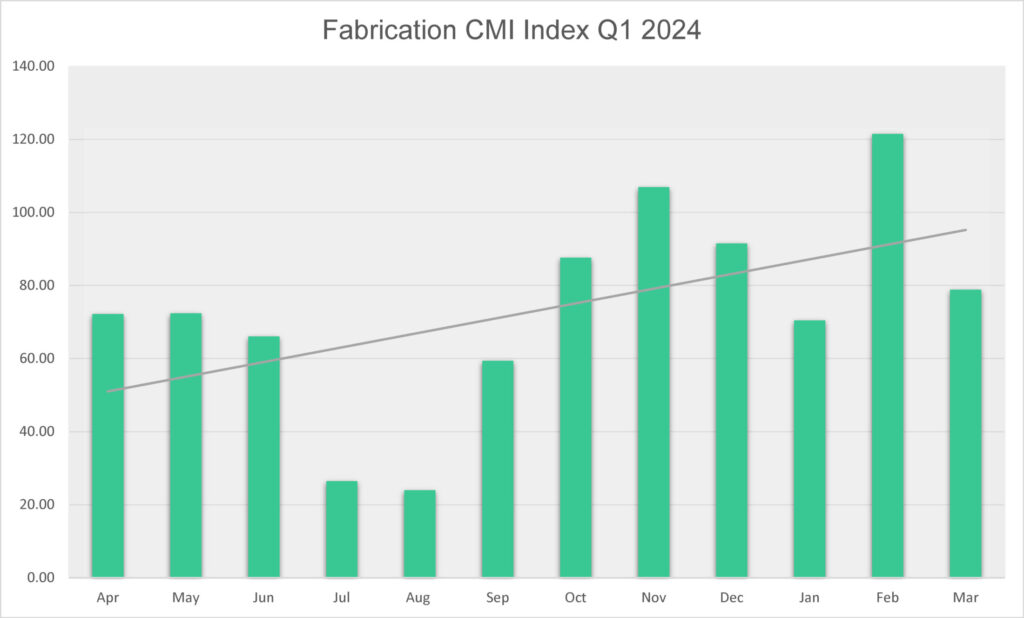

The latest Contract Manufacturing Index shows that the UK market for subcontract manufacturing, including fabrication and sheet metal working, continued to grow in the first quarter. The index was up 4.5% in the first three months of 2024, building on the strong upswing at the end of 2023. Fabrication represented 49% of the market.

Projects and budgets that had been on hold continue to be unlocked as orders are being placed and suppliers are busy quoting for work. February was the strongest month since March 2023.

Lead times in January and February dropped from the average of 22 days to 18 days, but lengthened again to 21 days in March.

Overall, the market remains around 30% below where it was a year ago.

The CMI is produced by sourcing specialist Qimtek and reflects the total purchasing budget for outsourced manufacturing of companies looking to place business in any given month. This represents a sample of over 4,000 companies who could be placing business that together have a purchasing budget of more than £3.4bn and a supplier base of over 7,000 companies with a verified turnover in excess of £25bn.

The baseline for the index is 100, which represents the average size of the subcontract manufacturing market between 2014 and 2018.

The CMI for Q1 2024 was 82 compared to 78.5 for the previous quarter and 117 for Q1 2023.

The largest single sector remains Industrial Machinery, which has been the number one sector for the past three years. The value of this sector almost doubled this quarter compared to the previous quarter. The second biggest sector was Construction, followed by items destined for the Electronics sector and Food & Beverage.

Commenting on the figures, Qimtek owner Karl Wigart said: “It was a good quarter with lots of projects that had been promised but delayed in the second half of last year finally coming on stream. Suppliers have been very busy quoting on new projects and both buyers and suppliers are very active. Suppliers recognise the need to seize these opportunities, which is evident in the reduced lead times.”