The latest Contract Manufacturing Index (CMI) shows that the UK subcontract manufacturing market surged by 60% in the first three months of 2023 compared to the previous quarter. As political and economic uncertainty eased, high value purchasing organisation came back to the market and the release of pent up demand saw activity soar.

- Market up 60% from previous quarter

- Release of pent up demand drives growth

The market jumped by 178% from December 2022 to January 2023 and remained healthy for the rest of the quarter.

Overall the first quarter of 2023 was 31% higher than the first quarter of 2022, demonstrating consistent growth in the longer term.

The CMI is produced by sourcing specialist Quimtek and reflects the total purchasing budget for outsourced manufacturing of companies looking to place business in any given month. This represents a sample of over 4,000 companies that could be placing businesses that together have a purchasing budget of more than £3.4bn and a supplier base of over 7,000 companies with a verified turnover of over £25bn.

The baseline for the index is 100, which represents the average size of the subcontract manufacturing market between 2014 and 2018.

The CMI for Q1 2023 was 117 compared to 73 for Q4 2022 and 89 for Q1 2022.

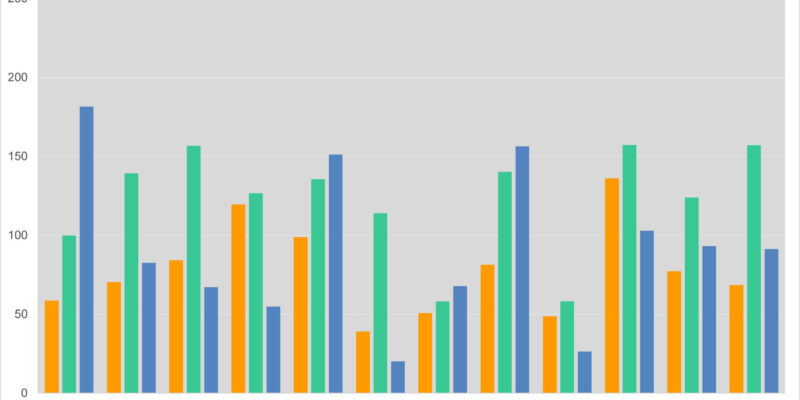

On a process by process basis the biggest growth in Q1 2023 was in fabrication, which grew by 71%. Machining grew by 56% and other processes by 15%. Fabrication represented 55% of the market, with machining on 38% and other processes on 7%.

The strongest market sectors have remained remarkably consistent over the past year, with Industrial Machinery and Food and Beverage holding the top two spots. Industrial Machinery has now been the strongest sector since the third quarter of 2021. The total value of the sector has more or less followed the trends in the CMI. This was evident in the latest figures where it grew by 130% compared to the previous quarter.

Food and Beverage has been the second largest sector since the second quarter of last year, but dropped back by 23% in Q1 2023 compared to Q4 2022.

Other notable changes in the quarter included Construction more than doubling in value and Electronics nearly three times higher. (Please note, this refers to items destined for the electronics industry, such as fabricated enclosures, rather than just electronic assembly).

The third largest sector was ‘Other’ demonstrating that the market is strong across the board.

Commenting on the figures, Qimtek owner Karl Wigart said: “Coming off a poor end to 2022 we expected January to be a bumper month and it certainly delivered. Overall it was a very good quarter. We have seen an increase in activity across the board with more projects, more contracts awarded, better award values and more activity by manufacturers in responding to RFQs.

“We know it is not an easy business climate at the moment, but everyone seems to be active and trying to do something about it.”