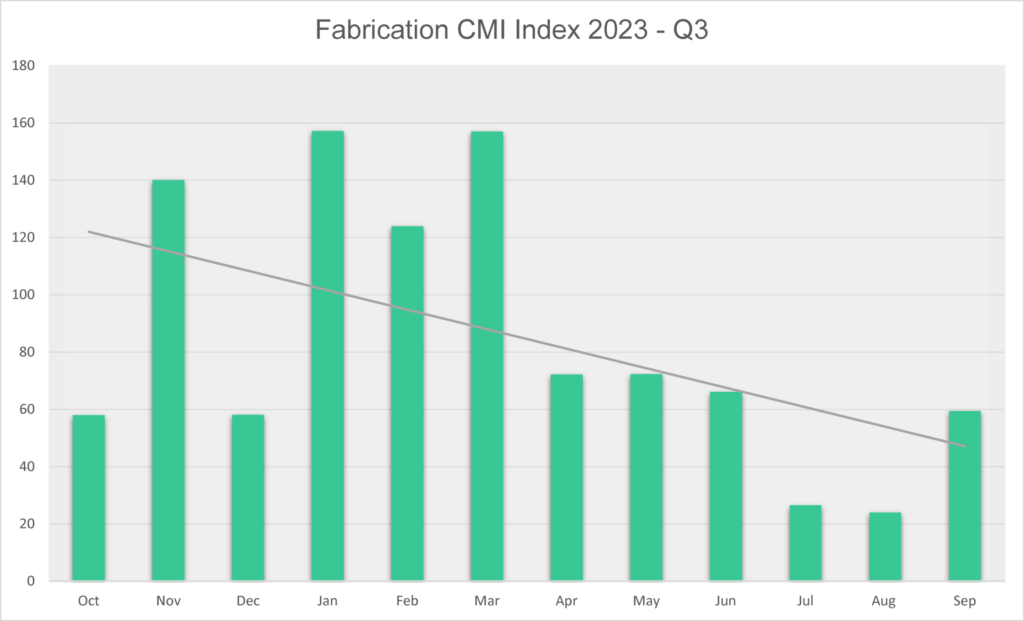

The latest Contract Manufacturing Index (CMI) shows that the number of companies looking to place new subcontract manufacturing business is at the lowest level since the index began in 2015. The market was 51% lower in the third quarter of 2023 than in the second quarter.

- Market down 51% on previous quarter

- Number of companies looking to place new subcontract business lowest since 2015

The new order pipeline has stalled as companies continue to push projects back month on month in the face of continuing market uncertainty.

The outlook improved slightly in September after two very poor months in July and August. The value of the contracts that are being awarded has gone up as has the percentage of contracts being awarded.

Overall the market was 63% down on the equivalent period in 2022.

The CMI is produced by sourcing specialist Qimtek and reflects the total purchasing budget for outsourced manufacturing of companies looking to place business in any given month. This represents a sample of over 4,000 companies who could be placing business that together have a purchasing budget of more than £3.4bn and a supplier base of over 7,000 companies with a verified turnover in excess of £25bn.

The baseline for the index is 100, which represents the average size of the subcontract manufacturing market between 2014 and 2018.

The CMI for Q3 2023 was 38 compared to 77 in Q2 2023 and 102 for Q3 2022.

On a process-by-process basis, the split of work remained fairly steady – although the volume of work fell dramatically. Machining accounted for 50% of new business as compared to 49% in the previous quarter, with fabrication up from 40% to 42%. Oher processes, including moulding and electronic assembly fell back from 10% of the market to 7%.

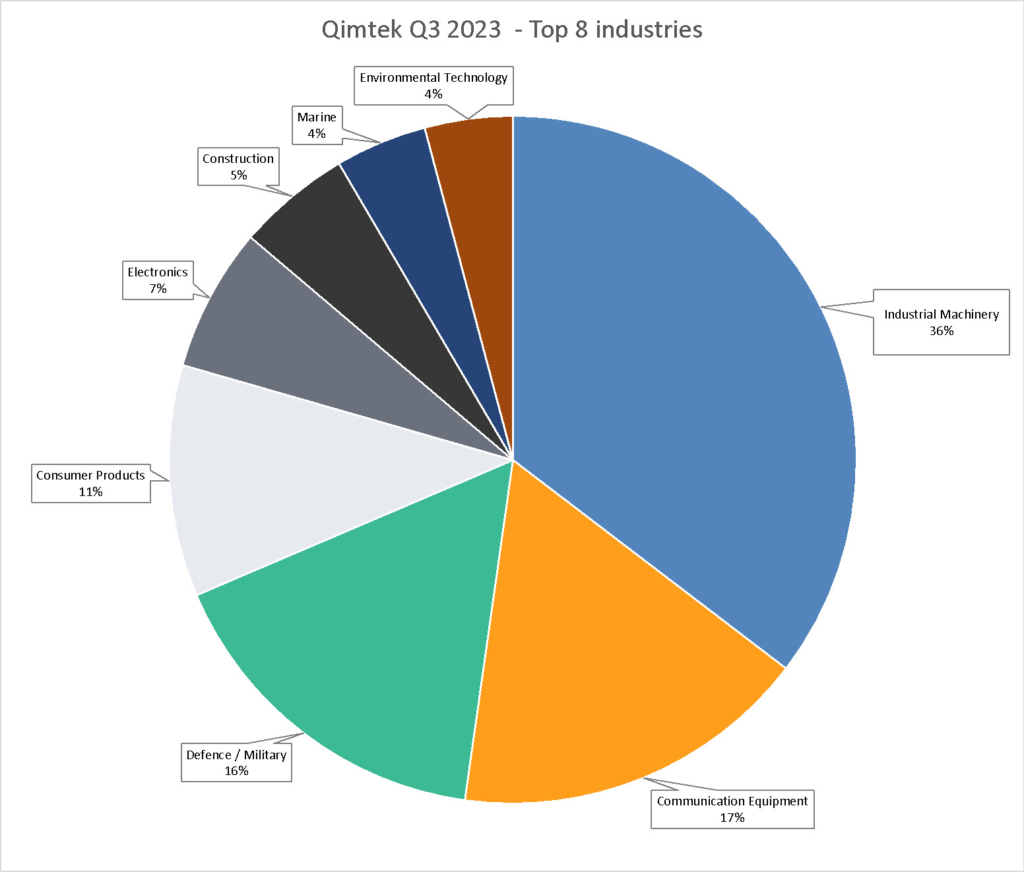

The largest single sector for the third successive quarter was Industrial Machinery, which only dropped by comparatively modest 8%. The second largest market was Communication Equipment, which more than doubled from the previous quarter, albeit from a fairly low base. The third largest market was Defence, which had not been a significant sector in the previous quarter. The biggest fallers were Construction and Marine.

Commenting on the figures, Qimtek owner Karl Wigart said: “These are disappointing figures – in line with other indices but lower than I had expected. Business was very slow in July and August, but showed signs of picking up in September.

“Companies seem to keep pushing promised projects into the future month after month. We saw fewer projects this quarter than in the earlier part of the year and fewer than in the equivalent period last year.

“We need to be cautious about being too optimistic, but we can only hope that the anticipated projects will start coming through in the remainder of the year. On the plus side, the value of the projects that have been awarded, and the percentage of projects being awarded, has gone up.”